The IRD’s latest guidance – updates and practical insights after two years of implementation

Covered income

Q:

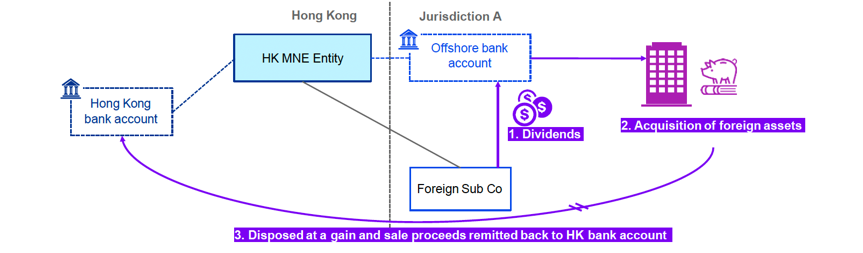

An unremitted specified foreign-sourced income has been applied to acquire immovable or movable property located outside Hong Kong and the property is subsequently sold. Assuming the conditions for tax exemption are not satisfied, will the sales proceeds still be regarded as the original specified foreign-sourced income and, therefore, need to be tracked and then subject to tax in Hong Kong when the proceeds are ultimately remitted back to Hong Kong, regardless of how many times such proceeds have been reinvested to acquire other immovable or movable property? If yes, how the gains or losses on the disposal of any such property are to be treated in determining the amount of the original specified foreign-sourced income that will be subject to the FSIE regime in Hong Kong?

A:

The sales proceeds from the subsequent disposal of immovable or movable property will still be regarded as the original specified foreign-sourced income and thus have to be tracked. When the sales proceeds are remitted to Hong Kong, the original specified foreign-sourced income will be regarded as received in Hong Kong and chargeable to profits tax in Hong Kong in case the conditions for tax exemption are not satisfied.

The amount of the original specified foreign-sourced income should not be altered by the subsequent acquisition and disposal of assets no matter whether gains or losses are generated from such reinvestment activities. Whether the gains or losses from the subsequent disposal of assets are chargeable to profits tax under the FSIE regime will be considered separately, having regard to the facts and circumstances relating to the disposal.

Economic Substance Requirement

Q:

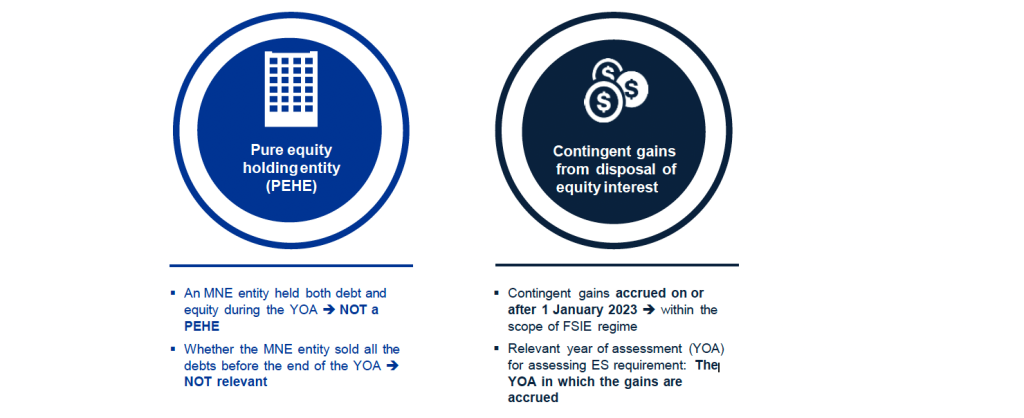

Company A disposed of certain equity interests and accrued a disposal gain in 2022. According to the disposal agreement, it would receive an additional sum subject to the business performance of the disposed entity. In 2023, Company A accrued and received the “contingent” disposal gain as the target performance was achieved. Does the contingent disposal gain accrued and received after 1 January 2023 fall within the scope of the FSIE regime notwithstanding that the disposal took place in 2022? If yes, what is the timing for considering the economic substance requirement? If Company A no longer maintained economic substance in Hong Kong subsequent to the disposal in 2022, would IRD take into account Company A’s economic substance in 2022, given that the disposal took place in 2022?

A:

The contingent disposal gain which accrued to Company A on or after 1 January 2023 falls within the scope of specified foreign-sourced income under the FSIE regime. The wording of section 15K(2) of the IRO is clear. The reference period for considering whether the economic substance requirement is met is the basis period of the year of assessment in which the specified foreign-sourced income accrues to an MNE entity. If Company A did not have any economic substance in Hong Kong during the year of assessment in which the contingent disposal gain accrued to it, the economic substance requirement would not be regarded as satisfied.

Q:

Company A closed its accounts on 31 December and held certain debts and equity interests. It disposed of all the debts on 1 June 2023 and only held equity interests afterwards. It derived offshore dividends at various times during the year 2023. Can it be regarded as a pure equity-holding entity and rely on the reduced economic substance requirement for all the dividends accrued during the year of assessment 2023/24?

A:

Section 15K(2) of the IRO provides different sets of conditions for pure equity-holding entities and non-pure equity-holding entities respectively in determining whether an entity satisfies the economic substance requirement during the basis period of the year of assessment in which the income accrues to the entity. For a pure equity-holding entity, the reduced economic substance requirement is applicable. Since Company A had held certain debts during the basis period of the year of assessment 2023/24 in which the dividends accrued to it, Company A could not be regarded as a pure equity-holding entity during the year even though all the debts were disposed of on 1 June 2023. Thus, the reduced economic substance requirement would not be applicable to it.

Participation requirement

Q:

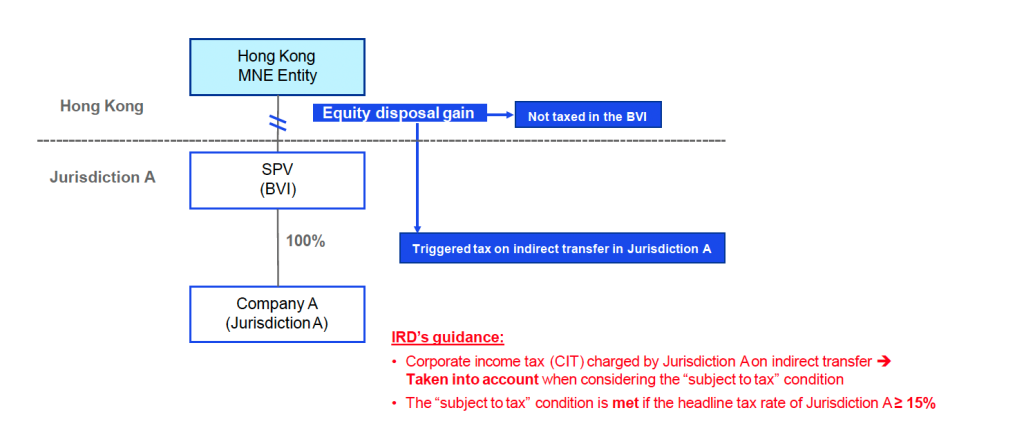

Company HK’s disposal of equity interests in Company X located in Jurisdiction X results in an indirect transfer of Subsidiary A, a foreign subsidiary indirectly held by Company HK in Jurisdiction A. Company HK is subject to indirect transfer tax (which is a corporate income tax) on the disposal in Jurisdiction A. If the statutory corporate income tax rate in Jurisdiction A is 25%, can the “subject to tax” condition be regarded as satisfied?

A:

If the specified foreign-sourced income is a gain derived from disposal of equity interests in an investee entity, the participation exemption only applies if the disposal gain is subject to a qualifying similar tax in a territory outside Hong Kong (foreign jurisdiction). The foreign jurisdiction may not necessarily be the jurisdiction in which the investee entity is located.

If the gain from disposal of the equity interests in Company X is subject to corporate income tax in Jurisdiction A on the indirect transfer of Subsidiary A, such tax would be taken into account in determining whether the “subject to tax” condition is satisfied in respect of the equity interest disposal gain. As the headline tax rate in Jurisdiction A is higher than the reference rate of 15%, the “subject to tax” condition would be regarded as satisfied.

Q:

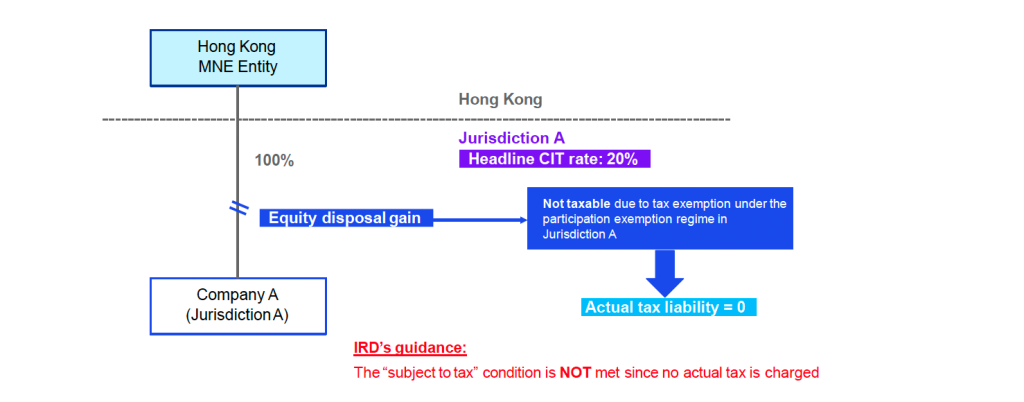

Company HK derived gains from disposal of its subsidiaries in Jurisdiction A. The gains were exempt from tax in Jurisdiction A pursuant to a participation exemption regime there. Will the “subject to tax” condition be regarded as satisfied in respect of the equity interest disposal gains?

A:

If no tax is charged on the gains derived by Company HK from the disposal of its subsidiaries, such disposal gains will not be regarded as subject to a qualifying similar tax in Jurisdiction A.

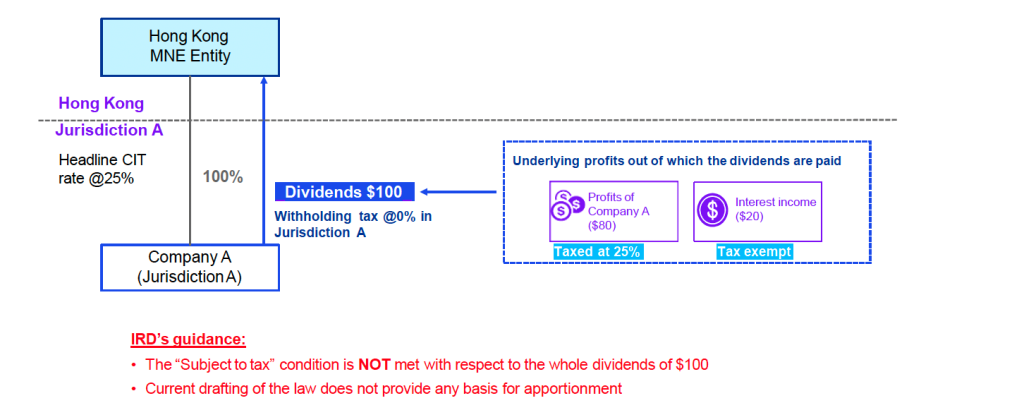

Q:

Company HK received a dividend of $100 from its wholly-owned subsidiary, Company A, which is located in Jurisdiction A. The dividend was not subject to any withholding tax in Jurisdiction A. The underlying profits out of which the dividend was distributed by Company A to Company HK consisted of:

|

(a) |

dividends received by Company A from its subsidiaries in the amount of $80, in respect of which the underlying profits had been subject to corporate income tax at a rate of not less than 15% in territories outside Hong Kong; and |

|

|

(b) |

interest income of $20 which was tax-exempt in Jurisdiction A. |

|

Would IRD accept an apportionment approach when ascertaining whether the dividend received by Company HK meets the “subject to tax” condition – i.e. the portion of dividend that was paid out from item (a) above (i.e. $80) would be regarded as fulfilling the “subject to tax” condition whereas the remaining portion that was paid out from item (b) (i.e. $20) would not?

A:

For dividend income, the “subject to tax” condition will only be met if one of the following conditions is satisfied:

|

(i) |

The dividend is subject to a qualifying similar tax in a foreign jurisdiction; |

|

(ii) |

The underlying profits of the dividend are subject to a qualifying similar tax in a foreign jurisdiction, and the amount of the profits is equal to or larger than that of the dividend; or |

|

(iii) |

If the underlying profits consist wholly or partly of dividends, one or more items of the related downstream income of the profits are subject to a qualifying similar tax in a foreign jurisdiction and the aggregate amount of all such items of income is equal to or larger than the amount of the dividend.

|

In the given scenario, (i) the subject dividend was not subject to tax in Jurisdiction A; (ii) the amount of the underlying profits (i.e. the profits of Company A) of the subject dividend which had been subject to a qualifying similar tax (i.e. $80) is smaller than that of the subject dividend; and (iii) there is no information showing that any related downstream income of the underlying profits had been subject to tax. In such circumstance, the “subject to tax” condition in respect of the subject dividend would not be regarded as met since none of the conditions provided in section 15N(2) of the IRO is satisfied.

Section 15N(2) of the IRO clearly provides that where the “subject to tax” condition is to be met in relation to a dividend for the reason that the underlying profits or related downstream income of the profits is subject to a qualifying similar tax, the amount or aggregate amount of such profits or income must be equal to or larger than the amount of the dividend. There is no room for the adoption of the apportionment approach when ascertaining whether the “subject to tax” condition is met.

Sources : Hong Kong Inland Revenue Department and Hong Kong Taxation Institution